Star Micronics ANNUAL REPORT 2023

TO OUR SHAREHOLDERS

Building a Foundation for Change

In 2023, operating results in both the Machine Tools and Special Products segments were weak, with a downturn in sales and significantly lower profits compared with the previous year. This was mainly due to growing concerns surrounding the threat of an economic recession owing to such factors as the prolonged upswing in interest rates in the U.S. and Europe as well as deteriorating market conditions and slowing investment in China. Moving forward, the outlook for the future remains uncertain.

2024 is the final year of our First Medium-Term Management Plan, a roadmap for building a foundation for change over the three-year period from 2022 to 2024. Recognizing the need to further solidify our foundation, we will redouble efforts to bring about a sustainable society and enhance corporate value by putting into practice our corporate philosophy, growing together with employees, and contributing to society.

Mamoru Sato

Representative Director,

President and CEO

01Operating Results in 2023

Looking at 2023, the outlook for the economy remained uncertain throughout the period under review. Despite an overall modest recovery amid signs of a lull in the surge in resource prices and prolonged inflation, this uncertainty largely reflects growing concerns surrounding the threat of an economic recession owing to the prolonged upswing in interest rates in the U.S. and Europe, deteriorating market conditions and slowing investment in China, and fluctuations in foreign currency exchange rates.

In each of the major markets in which the Star Micronics Group operates, demand for POS printers was generally weak. In addition, demand for the Group’s mainstay machine tools in overseas markets, which had previously remained high, stalled with little or no forward momentum. Exacerbating these difficult trends, demand in Japan also failed to recover.

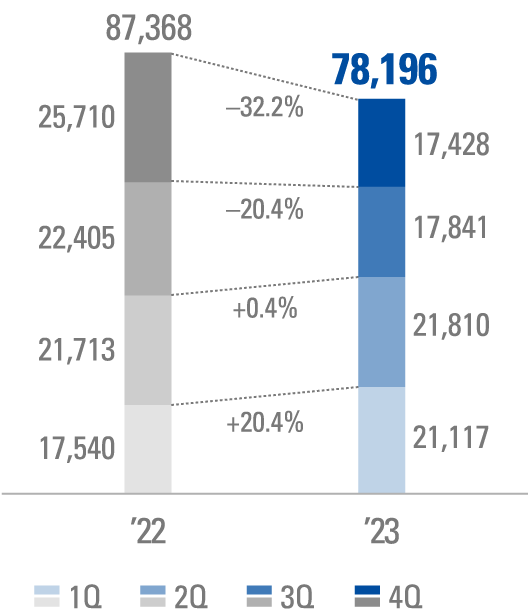

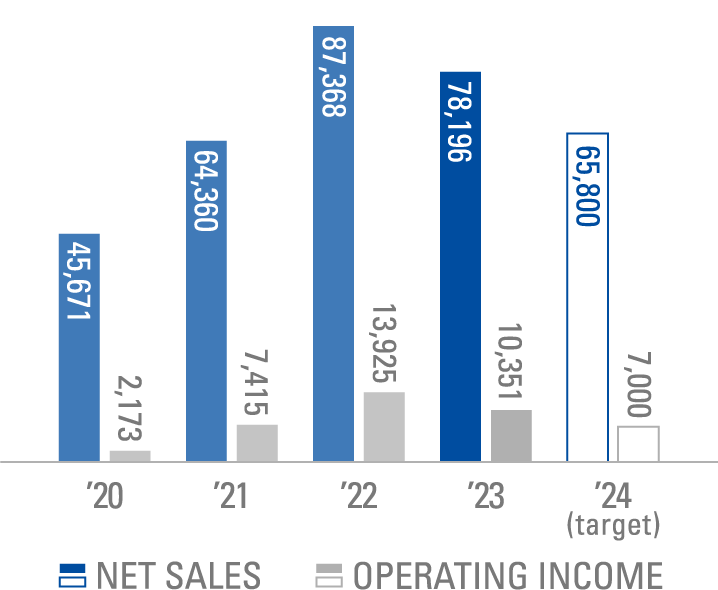

Under these circumstances, the Star Micronics Group reported net sales of ¥78,196 million for the year under review, down 10.5% compared with the previous year. Despite the overall impact of depreciation in the value of the yen, this was mainly due to a decline in sales of the Company’s mainstay machine tools. From a profit perspective, operating income declined 25.7%, to ¥10,351 million. Net income attributable to owners of the parent fell 20.6%, to ¥8,175 million.

Meanwhile, Smart Solution Technology, Inc. (SST) was included in the Company’s scope of consolidation and the Special Products Segment effective from the year under review.

NET SALES(Millions of yen, %)

02Business Overview

In the Machine Tools Segment, sales of CNC automatic lathes decreased. Notwithstanding progress from the beginning of the year under review to reduce the order backlog from the previous year mainly in the U.S. and European markets, this decrease was ostensibly due to delays in market recovery in China. By geographic region, sales in the U.S. declined overall owing to sluggish market conditions, which largely reflected such factors as the prolonged upswing in interest rates. In addition, sales in the European market increased significantly centered mainly on automotive-related products. Meanwhile, sales decreased substantially in the Asian market. This was essentially attributable to weak sales of automotive- and telecommunications-related products on the back of the continued cautious approach toward capital investment in China over the latter half of the previous year and other factors. Sales declined significantly in the domestic market, for the most part due to the continued lackluster performance of the automotive sector.

Accounting for each of the aforementioned factors, sales and income declined year on year. In specific terms, sales decreased 10.6% compared with the previous year, to ¥62,085 million. Operating income declined 15.5%, to ¥10,350 million.

Turning to the Special Products Segment, sales of POS printers declined. This largely reflected the downturn in mPOS demand, which had remained robust. Looking at trends by geographic region, sales in the U.S. market decreased substantially owing to the downturn in mPOS demand. Sales in the European market were essentially unchanged from the previous year due to the impact of such factors as the yen’s depreciation. Meanwhile, despite weak market conditions throughout the domestic market, sales in Japan increased significantly compared with the previous year owing to the inclusion of SST in the Company’s scope of consolidation.

Accounting for these factors, sales decreased 10.3% compared with the previous year, to ¥16,111 million. Operating income declined substantially year on year, to ¥1,953 million, down 48.0%.

03Outlook for the Following Year

Looking ahead, conditions throughout the global economy are expected to remain uncertain. In addition to ongoing concerns surrounding such geopolitical risks as the prolonged crisis in Ukraine and military conflicts in the Middle East, this is due to a variety of factors, including anxieties toward a slowdown in economic activities owing to the impacts of continued inflation and the tightening of global monetary policy.

Under these circumstances, and in the context of the Company’s consolidated business performance for the coming year, sales in the mainstay Machine Tools Segment are forecast to decline. Despite expectations of a recovery mainly for automotive-related products in Japan and an anticipated gradual positive turnaround overseas toward the latter half of the coming year, this forecast decline is amid sluggish capital investment demand across all regions since the previous year. In the Special Products Segment, sales are projected to decline. While sales are expected to increase due to new products, this forecast downturn largely reflects the overall weak nature of market conditions especially in the U.S.

Taking into account the aforementioned factors, our outlook for consolidated results in the coming year is a downturn. In specific terms, we expect a decrease in net sales of 15.9% compared with the year under review, to ¥65,800 million. On a year-on-year basis, operating income is forecast to decline 32.4%, to ¥7,000 million and net income attributable to owners of the parent to also drop 37.6%, to ¥5,100 million in the year ending December 31, 2024.

Forecasts are based on the assumptions that the yen/US dollar exchange rate will be JPY135 and the yen/Euro exchange rate will be JPY150.

NET SALES AND

OPERATING INCOME(Millions of yen)

04About the Medium-Term Management Plan

The Star Micronics Group formulated its Medium-Term Management Plan in 2022 as part of a review of its Corporate Philosophy, Purpose, Management Policy, and Action Guidelines to empower employees to make decisions and act autonomously as it seeks to become a company that grows sustainably together with society. At the same time, we formulated a Vision for 2030. (Please refer to the Company’s Medium-Term Management Plan for details.)

In order to realize its Vision for 2030, the Company has divided the next nine years into three-year periods. In working toward “building a foundation for change,” “driving change,” and “realizing our vision” over each period, respectively, Star Micronics has formulated the first Medium-Term Management Plan covering the three years from 2022 to 2024. Details of issues to be addressed and progress in 2023, the second year of the Company’s First Medium-Term Management Plan, are presented as follows.

Positioning the mPOS and food delivery markets as a principal area of operations, the Star Micronics Group will work to further expand sales of printers and peripheral equipment while at the same time refining software technologies in a bid to continue providing new value to customers. Through these means, the Group will endeavor to become a total solution provider for store operations in the Specialty Products Segment.

In 2023, the Star Micronics Group expanded its product lineup, including label printers and peripheral equipment, while undertaking plans for new products. Moving forward, the Group will further step up its new product planning activities.

In the Machine Tools Segment, the Group will strengthen the production system in Thailand and China, position the Kikugawa Factory as a sustainable factory that nurtures people, develops technology, and grows together with society and promote large-scale renovation in order to meet robust demand for facilities and equipment. At the same time, steps will be taken to delve deeper into hardware technologies and adopt software technologies, and to further cement the Group’s position as a leading manufacturer of automatic lathes.

In addition to the start of operations at the Asia Solution Center in Shanghai, steps were completed to upgrade and expand facilities and equipment at the Company’s factory in Thailand as a part of efforts to strengthen the production system. These initiatives were geared toward reinforcing sales in 2023. In 2024, plans are in place to establish a sales subsidiary in India with the aim of cultivating the Indian market. Moreover, renovation work is finally scheduled to comment at the Group’s Kikugawa Factory.

As far as new business is concerned, the Group will focus on uncovering opportunities in the three production DX, store DX, and logistics DX domains while aiming to construct a new business model mainly through M&As.

In 2023, Star Micronics completed steps to include SST, a company with strengths in software and system development, in the Company’s scope of consolidation as a wholly owned subsidiary. To use this as a foothold to explore opportunities in each of the three DX domains, we will work to improve the DX capabilities of the entire Group and accelerate the pace of new business creation while incorporating SST’s technologies.

From a Group-wide perspective, energies will be directed toward strengthening the management platform, reforming human resource systems that allow employees to maximize their potential, and constructing R&D structures and systems to continuously create proprietary technologies, while vigorously moving forward with initiatives to address material issues based on the Sustainability Policy.

At the start of 2023, we launched the Development Headquarters and initiated activities in a bid to establish R&D structures and systems. As far as strengthening the management platform is concerned, we also established a designated department with management planning functions. In addition to further promoting these activities, we plan to put in place a new human resource structure and systems in 2024.

Positioned as KPIs, we are targeting cumulative operating cash flow of ¥20-¥25 billion, an average consolidated annual operating income per employee of ¥6 million, ROE of 10.0% or more, a ratio of R&D expenses to net sales of 5.0%, and non-consolidated annual education and training outlays per employee of ¥100,000 over the three-year period from 2022 to 2024. In the second year, 2023, operating cash flow came in at ¥7.1 billion on a single-year basis and ¥14.6 billion on a cumulative basis. On a single-year and average basis, consolidated annual operating income per employee, ROE, the ratio of R&D expenses to net sales, and education and training outlays per employee came in at ¥6.19 million and ¥7.28 million, 10.7% and 13.1%, 2.4% and 2.3%, and ¥70 thousand and ¥80 thousand, respectively.

We will continue to aggressively reform our business and management on an ongoing basis and make concerted Group-wide efforts to enhance our corporate value.

05Corporate Governance and Shareholder Returns

The Board of Directors of the Company consists of three internal directors and four outside directors, and thus the outside directors already account for the majority. Star Micronics has also put in place the non-mandatory Nomination and Compensation Committee as an advisory body to the Board of Directors to enhance the transparency and objectivity of procedures related to the nomination and compensation of directors and executive officers and to further enhance corporate governance.

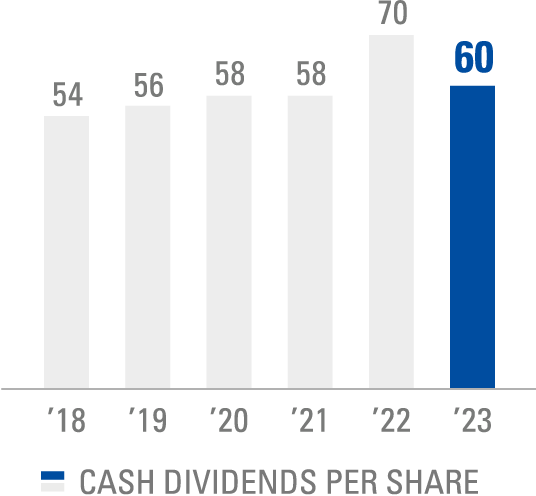

Star Micronics positions the return and distribution of profits to shareholders as an important management priority. Our basic policy is to maintain payment of a progressive and stable annual dividend of at least ¥60 per share as well as a consolidated total payout ratio of at least 50%, including the repurchase of own shares.

Guided by this policy, Star Micronics plans to pay a period-end dividend of ¥30 per share. Coupled with the interim dividend of ¥30 per share, the Company will pay an annual dividend of ¥60 per share for the year under review, unchanged from the previous year, excluding the previous year’s special dividend.

Looking ahead, and once again in line with its policy, Star Micronics plans to pay an interim and period-end dividend of ¥30 per share for an annual dividend of ¥60 per share for 2024.

As far as the Company’s internal reserves are concerned, Star Micronics is committed to enhancing its corporate value while increasing shareholders’ profits. At the same time, the Company will look to engage in a variety of activities including investment in future growth fields in a bid to ensure its sustainable growth.

In working toward achieving its established goals, the Star Micronics Group kindly requests the continued support and understanding of all stakeholders.

March 2024

Mamoru Sato

Representative Director, President and CEO

CASH DIVIDENDS

PER SHARE(Yen)